As widely expected, the Swiss National Bank (SNB) sees no need for action despite inflation concerns caused by geopolitical tensions and is keeping its key interest rate unchanged at 0%. The sharp rise in oil prices to over USD 100 per barrel is stoking new global inflation concerns and is a reminder of the situation in 2022/2023, when some regions temporarily experienced double-digit inflation rates and monetary policy measures were applied too late in certain cases. However, the current situation also differs significantly from the energy crisis back then. In 2022, several shocks overlapped: pent-up demand after lockdowns, disrupted supply chains, and soaring gas prices due to the war in Ukraine.

Until the onset of the Iran conflict, deflationary tendencies shaped Switzerland as a result of the strong Swiss franc, resulting in low inflation near zero. Compared to other central banks, the SNB is therefore in a relatively comfortable position, making a wait-and-see approach probably the best decision for the time being.

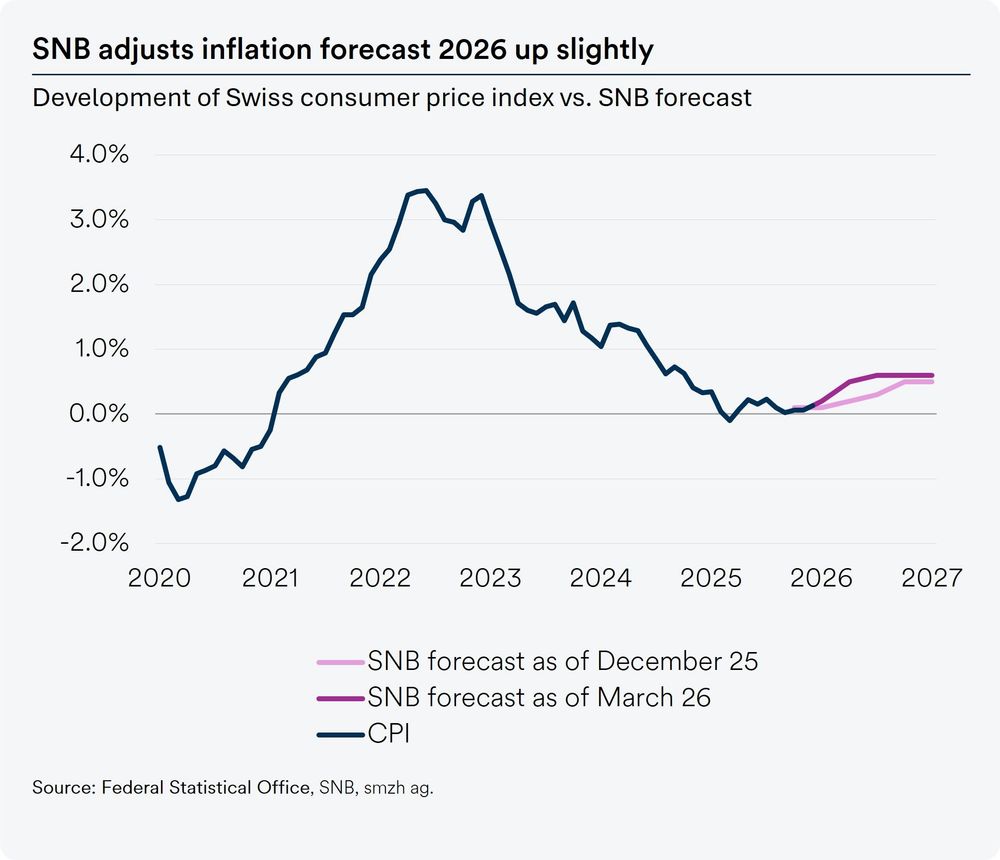

Downward pressure on inflation has eased

The question now is how persistent this new price pressure actually is. An inflationary surge due to higher energy prices would mainly increase import prices in Switzerland. This kind of inflation is less problematic and would, in part, be offset by a strengthening franc. Only if the price shock spills over into other segments through second-round effects and pushes up core inflation could monetary intervention make sense. Given that current inflation is at the lower end of the SNB’s target range of 0 to 2%, the SNB has sufficient leeway to wait and continue monitoring the situation.